-

1 Introduction

The place of human rights and investor obligations in the universe of international investment agreements (IIAs) has long been a topical issue in academic and non-academic discussions. It is often argued that the recognition of investors’ human rights obligations and more far-reaching reforms aimed at making the regime fully human rights-friendly are highly necessary. Otherwise, any changes in the international investment regime will not be able to strike a balance between competing interests of foreign investors and other actors in an investment dispute.1x B. Choudhury, ‘Investor Obligations for Human Rights’, 35 ICSID Review 82, at 103-4 (2020) and A. Arcuri and F. Violi, ‘Human Rights and Investor-State Dispute Settlement: Changing (Almost) Everything, So that Everything Stays the Same?’, 3 Diritti umani e diritto internazionale 579, at 596 (2019). So far, it has been proven that shallow or preambular references in IIAs to human rights concerns in different contexts, e.g. corporate social responsibility (CSR), the protection of public interest or the state right to regulate, can hardly entail obligations on foreign investors.2x M. Krajewski, ‘Human Rights in International Investment Law: Recent Trends in Arbitration and Treaty-Making Practice’, SSRN Scholarly Paper, at 8 (2018) and L. Choukroune, ‘Corporate Social Responsibility and Foreign Direct Investment – The Indian Investment Treaty Approach and Beyond’, 2 Transnational Dispute Management , at 7 (2018). It has been repeatedly shown that reliance on interpretative techniques and systemic integration does not suffice to harmonise human rights law and investment law.3x J. Coleman et al., ‘Human Rights Law and the Investment Treaty Regime’, Columbia Center on Sustainable Investment Working Paper 2019:7; J. Linarelli et al., The Misery of International Law: Confrontations with Injustice in the Global Economy (2018), at 161. Straightforward incorporation of human rights-related obligations on foreign investors has been considered as an option, without which the investment regime and its reform efforts will remain incomplete.4x Choudhury, above n. 1, at 83.

Imposing obligations on foreign investors in IIAs could be a reform option that can help address the issue of the asymmetrical structure in the international investment regime.5x While the asymmetry in international investment law regime has different faces, for the purposes of this study, asymmetry in investment law is understood substantively. Specifically, the primary purpose of the regime is to protect and promote foreign investment. To this end, foreign investors are provided with various rights and standards of protection. However, neither home or host states nor local communities and NGOs who may be adversely affected by foreign investments or who have an interest in the settlement of disputes between foreign investors and states can enjoy such rights and protections. Therefore, by placing foreign investors in a privileged position, the regime creates an asymmetrical relationship between foreign investors and other stakeholders in international investment relations. Balancing the overprotected and privileged position of foreign investors has been one of the most widely advocated courses of action in the literature to fix the investment regime’s legitimacy deficits.6x ‘An Open Letter to the Chair of UNCITRAL Working Group III and to All Participating States Concerning the Reform of Investor-State Dispute Settlement: Addressing the Asymmetry of ISDS’ www.eur.nl/en/news/erasmus-institute-public-knowledge (last visited 19 June 2021). To this end, the introduction of more and effective human rights-related obligations on investors has been considered as one such reform option that can contribute to the balancing of different interests within the investment law regime.7x P. Dumberry and G. Dumas-Aubin, ‘How to Impose Human Rights Obligations on Corporations Under Investment Treaties? Pragmatic Guidelines for the Amendment of BITs’, in K.P. Sauvant (ed.), Yearbook on International Investment Law and Policy 2011-2012 (2013) 569. There are already some studies on investor obligations provisions in IIAs, but much remains unknown about their characteristics and how many of them there are. Without knowing the precise extent and nature of these existing obligations, it is unlikely that any reform effort focusing on the place of investor obligations in IIAs will be successful in establishing the balance. After all, how could effective reform proposals concerning investor obligations be formulated if we do not know which features of the existing obligations need what kind of reform?

While several studies have focused on human rights-related investor obligations in some agreements,8x See e.g.: M. Krajewski, ‘A Nightmare or a Noble Dream? Establishing Investor Obligations Through Treaty-Making and Treaty-Application’, 5 Business and Human Rights Journal 105 (2020); Choudhury, above n. 1; P. Dumberry and G. Dumas-Aubin, ‘A Few Pragmatic Observations on How BITs Should Be Modified to Incorporate Human Rights Obligations’, 11 Transnational Dispute Management 1 (2014). a comprehensive analysis of all the existing IIAs has not yet been conducted. Traditional content analysis methods are unsuitable to process vast amounts of legal data,9x W. Alschner and D. Skougarevskiy, ‘Mapping the Universe of International Investment Agreements’, 19 Journal of International Economic Law 561, at 562 (2016). and conducting a traditional content analysis on all the IIAs would be immensely daunting. In this regard, the emerging field of computational international legal research can be of great use.10x For a more detailed analysis, see: W. Alschner, ‘The Computational Analysis of International Law’, in R. Deplano and N. Tsagourias (eds.), Research Methods in International Law: A Handbook (2021) 203. Thanks to the rise of the use of computational methods in social sciences and legal research, questions that were simply unanswerable or extremely time- and resource-consuming before, have become answerable. International economic law is one of the fields where there is ample opportunity for computational methods to make significant and original contributions.11x For a more detailed analysis, see: W. Alschner, J. Pauwelyn & S. Puig, ‘The Data-Driven Future of International Economic Law’, 20 Journal of International Economic Law 217 (2017). Drawing on these methods, I aim to add granularity to our knowledge of patterns and features concerning the provisions on human rights-related investor obligations in IIAs. I analyse whether these obligations can address criticisms concerning the substantively asymmetrical structure of the international investment law regime that grants foreign investors far-reaching rights without any corresponding obligations. In this light, the main research question of this study is the following: what is the state of the art regarding human rights-related investor obligations in IIAs, and how can they be evaluated in terms of their potential to balance the asymmetries between rights and obligations of foreign investors and other stakeholders12x This study adopts the definition of ‘stakeholders in investment arbitration’ proposed by Vargiu. He defines ‘stakeholders’ as actors with ‘a tangible interest in how investment treaties are interpreted and applied, and how international investment law is developed ’. In addition to state parties and foreign investors in a dispute, he considers ‘other states involved in investment relationships with foreign investors, investors that may at any point file a claim before an investment arbitral tribunal, scholars who analyse the case-law and teach the next generation of investment lawyers, NGOs and associations interested in the subject matter of the cases, and the taxpayers of each state acting as respondent before an arbitral tribunal’ as stakeholders. See: P. Vargiu, ‘Stakeholders of Investment Arbitration: Establishing a Dialogue Among Arbitrators, States, Investors, Academics and Other Actors in International Investment Law’, in K.F. Gómez (ed.), Private Actors in International Investment Law (2021) 5, at 7. in foreign investment relations?

The computational analysis in this study is conducted on the basis of an in-depth qualitative analysis. Drawing on the vast existing literature in international investment law and on legal doctrinal analysis, the study develops a taxonomy of the scope and depth of investors’ obligations in past and existing treaties. These obligations have been classified along five dimensions, namely 1) year when the IIA containing a given obligations was concluded, 2) location of the provision in the treaty text, 3) addressee of the provision, 4) strictness in the language of the provision and 5) subject matter of the obligations. In total, 3,558 IIAs, from 1948 to 2021, have been text-mined and, on the basis of the said taxonomy, an assessment of the developments of human rights-related obligations has been conducted. The combination of the computational method with qualitative analysis yields an original and nuanced mapping of the developments concerning the human rights-related obligations on investors in all IIAs.

This article will proceed, first, with a description of what is understood by ‘human rights-related’ investor obligations in IIAs (Section 2). Next, the methodology of this article will be explained in detail (Section 3), and the results of the automated textual analysis of the human rights-related investor obligations provisions in IIAs will be presented and discussed (Section 4). This quantitative analysis will be followed by an analysis of the identified provisions on human rights-related investor obligations on the basis of the taxonomy and along its different dimensions (Section 5). Section 6 will conclude. -

2 Human Rights-Related Investor Obligations

While human rights-related references are on the rise in newly concluded IIAs,13x K. Gordon, J. Pohl & M. Bouchard, ‘Investment Treaty Law, Sustainable Development and Responsible Business Conduct: A Fact-Finding Survey’, OECD Working Papers on International Investment 2014:01, at 5 and UNCTAD, ‘The Changing IIA Landscape: New Treaties and Recent Policy Developments’, IIA Issues Note 2020, at 9. another and more relevant development in IIA drafting for this study is that the number of provisions that impose direct or indirect human rights-related obligations on investors is also rising. Previously, such obligations could be derived from, for example, states’ domestic laws, investment contracts between states and foreign investors or investors’ political risk insurance policies. With the rise of these provisions in IIAs, these obligations have become elevated to the international level.14x K. Van der Ploeg, ‘Protection of Regulatory Autonomy and Investor Obligations: Latest Trends in Investment Treaty Design’, 51 International Lawyer 109, at 119 (2018). Increasingly, in new-generation IIAs and model bilateral investment treaties (BITs), one can find more provisions on human rights that apply not only to states but also to investors and investments.15x I. Seif, ‘Business and Human Rights in International Investment Law: Empirical Evidence’, in J. Chaisse, L. Choukroune & S. Jusoh (eds.), Handbook of International Investment Law and Policy (2020), at 3. However, these provisions do not come in one shape; rather, there are fundamental variations concerning their specific characteristics such as their language, location in an IIA, subject matter and addressee. They may deal with various subjects, be found in a treaty’s preamble or main text, be addressed directly to investors or states or employ language with different degrees of strictness. The following provisions from separate IIAs can illustrate this variety: ‘Investors shall uphold human rights in the workplace and the community in which they are located’16x Art. 14(2) Supplementary Act A/SA.3/12/08 Adopting Community Rules on Investment and the Modalities for Their Implementation with ECOWAS, 19 December 2008 (hereinafter ECOWAS Supplementary Act). or ‘The Parties shall encourage cooperation between enterprises in relation to goods, services and technologies that contribute to sustainable development and are beneficial to the environment’.17x Art. 10.8(1) Free Trade Agreement between the EFTA States and Georgia, 27 June 2016.

The term human rights-related obligations implies a broader category than direct human rights obligations on investors. An IIA provision may directly address foreign investors and concern a subject that is understood as a matter of human rights in its narrow sense. If a provision introduces a clear obligation about protection of environmental, human, labour and indigenous rights, it can be considered as imposing a direct human rights obligation on foreign investors. To illustrate, provisions stating that ‘Investments shall, in keeping with good practice requirements relating to the size and nature of the investment, maintain an environmental management system’18x Art. 18(1) Reciprocal Investment Promotion and Protection Agreement Between the Government of the Kingdom of Morocco and the Government of the Federal Republic of Nigeria, 3 December 2016. or ‘Investors and their investments shall comply with the labor and environment laws and regulations of the host contracting party with respect to management and operation of an investment’19x Art. 14 Agreement between the Government of the Federal Democratic Republic of Ethiopia and the Government of the State of Qatar for the Promotion and Protection of Investments, 14 November 2017. can be considered as creating direct obligations on investors.

Yet what makes a provision human rights-related is not just whether it is a matter of human rights in its narrow sense. IIA provisions can introduce responsibilities on investors that can exert a positive influence on the enjoyment of human rights in the host countries. These provisions are not confined to those directly referring to human rights. In fact, even if a provision addresses issues conceived of as ‘economic’, it can have indirect implications for the rights of individuals who are adversely affected by foreign investments.20x www.iisd.org/publications/integrating-investor-obligations-and-corporate-accountability-provisions-trade-and (last visited 5 December 2021). Take a provision on taxation. Only in recent years have human rights impacts of tax laws started to be recognised by human rights scholars, as well as by international organisations.21x N. Reisch, ‘Tax, Inequality, and Human Rights’, in P.G. Alston and N.R. Reisch (eds.), Taxation and Human Rights: Mapping the Landscape (2019) 34, at 34. In its general comment, the UN Committee on Economic, Social and Cultural Rights stated that states should combat abusive tax practices such as transfer pricing, tax evasion and tax avoidance for the realisation of economic and social rights.22x UN Committee on Economic, Social and Cultural Rights E/C.12/GC/24, 10 August 2017, at para 37. Similarly, a provision on corporate governance may create human rights-related consequences. It is argued that ‘human rights awareness and corporate policies have become part of the credo of “good” business.’23x C. Scheper, ‘“From Naming and Shaming to Knowing and Showing”: Human Rights and the Power of Corporate Practice’, 19 International Journal of Human Rights 737, at 737 (2015). A provision stipulating that ‘investors and their investments should develop their best efforts to … develop and implement good corporate governance practices’24x Art. 815(2)(f) Free Trade Agreement between the Republic of Chile and the Federative Republic of Brazil, 21 November 2018. may create obligations on foreign investors to refrain from abusive corporate governance practices that can violate the rights of individuals or groups of people. Or a provision stating that ‘[i]nvestors shall be subject to civil actions for liability in the judicial process of their host State for acts or decisions made in relation to the investment where such acts or decisions lead to significant damage, personal injuries or loss of life in the host State’25x Art. 17 ECOWAS Supplementary Act, above n. 16. may enable or improve the enjoyment of the right to access to justice for individuals who physically suffered from foreign investment operations. Such provisions on various subjects may ultimately mitigate adverse human rights impacts of foreign investments in their host states.

In order not to exclude such provisions from the analysis on investors’ obligations in IIAs, embracing the broader conceptualisation of ‘human rights-related’ instead of ‘human rights’ provisions is essential. An analysis focusing only on investor obligations provisions touching on human rights in its narrow sense or non-economic issues would result in ignoring many other provisions that can be interpreted by arbitrators as imposing human rights-related obligations on foreign investors.

Human rights-related investor obligations provisions show a high degree of variety in terms of the subject matter of the obligation:

Investor/investment definition conditioning domestic law compliance: One group of definitional provisions require investments and investors to have certain characteristics or perform certain tasks to benefit from investment treaty protections. When defining the scope, this group of IIA provisions require that, for instance, the term ‘investor’ means any legal person constituted under the host state’s laws and regulations. Similarly, these provisions may stipulate that for an investment to become eligible for protection, it needs to be made in compliance with the laws and regulations of the host state. Hence, in the case of non-compliance with domestic laws, an investor or investment may not be eligible for protection under these IIAs. In such cases, tribunals may even conclude that they do not have ratione personae or ratione materiae jurisdiction to decide on the dispute. Therefore, to enjoy IIA protections, investors and investments must comply with their host state’s domestic laws as prescribed by these IIAs. In a sense, without specifying it as an outright obligation on investors,26x N. Bernasconi-Osterwalder, ‘Inclusion of Investor Obligations and Corporate Accountability Provisions in Investment Agreements’, in J.J. Chaisse, L. Choukroune & S. Jusoh (eds.), Handbook of International Investment Law and Policy (2020), at 11. these definitional provisions can oblige investors to abide by the national laws. While most of these definitions require a pre-establishment obligation of compliance, some also impose a post-establishment obligation to comply with the host’s domestic laws.

Domestic law compliance: Similar to the definition clauses, another group of investor obligations provisions stipulate that protected investment shall be governed by or carried out according to the laws in force in the host state. These provisions, too, may impose pre- or post-establishment obligations on investors. Unlike the definitional provisions, these provisions do not prevent the exercise of jurisdiction by arbitral tribunals. Instead, tribunals may apply to these provisions in their considerations about the merits of a dispute at hand. These provisions internationalise the duty of investors to comply with domestic laws and may allow states to raise this before arbitral tribunals if investments do not comply with domestic laws. These provisions, and the definitional provisions requiring domestic law compliance, do not directly impose human rights-related obligations on investors. It is up to the legislatures of the host states to determine the exact scope of the obligations these provisions prescribe.27x Krajewski, above n. 8, at 119. Nevertheless, they may require investors to comply with, say, constitutional human rights protections or other human rights protections found in domestic legislation, insofar as these sources of human rights obligations are applicable to private enterprises.28x Ibid., 120. Moreover, compliance with domestic laws that aim to protect human rights, even if not explicitly referring to human rights, can fall within the scope of the obligation imposed by these provisions.29x Ibid. Here, for instance, legislation necessitating environmental and social impact assessments prior to investments or minimum wage regulations can be given as examples.

Tax/fiscal obligations: Some investor obligations provisions require investors to fulfil their tax and fiscal duties in their host states. Tax revenues constitute the majority of state income that is used to provide essential services such as health, education, housing, access to water and many other human rights.30x www.business-humanrights.org/en/blog/tax-avoidance-the-missing-link-in-business-human-rights/ (last visited 5 December 2021). Similarly, other fiscal and financial payments such as fees, charges or contractual undertakings are other important sources of revenue for states. However, in the context of investment relations, abusive tax practices such as tax evasion or tax avoidance or failure to fulfil other fiscal obligations by investors can deprive states of part of their precious public funds. Thus, investors’ failure to comply with their tax and fiscal obligations can have significant repercussions on the rights of individuals in their host states.31x S. Darcy, ‘“The Elephant in the Room”: Corporate Tax Avoidance & Business and Human Rights’, 2 Business and Human Rights Journal 1 (2017). For a more detailed analysis on different aspects of the relationship between tax, taxation and human rights, see: P.G. Alston and N.R. Reisch (eds.), Tax, Inequality, and Human Rights (2019).

Corporate governance: Some provisions concern how an investment is managed. How an enterprise is governed can have commercial consequences for the private entity itself, but it may also lead to human rights violations. In this sense, some IIA provisions link responsible business practices and good corporate governance either by encouraging or requiring enterprises to follow internationally recognised good corporate governance guidelines and standards or maintain, develop and apply good practices concerning corporate governance.32x Choudhury, above n. 1, at 91.

Anti-corruption: Corruption enables violations of various civil, political, economic, and social rights,33x www.unodc.org/e4j/en/anti-corruption/module-7/key-issues/impact-of-corruption-on-specific-human-rights.html (last visited 5 December 2021). and it is generally argued that it could and should be conceptualised as a human rights violation.34x A. Peters, ‘Corruption as a Violation of International Human Rights’, 29 European Journal of International Law 1251 (2018) and D. Hess, ‘Business, Corruption, and Human Rights: Towards a New Responsibility for Corporations to Combat Corruption’, 2017 Wisconsin Law Review 641 (2017). In this regard, a portion of IIAs provides for investors’ anti-corruption obligations. Accordingly, if an investment is made in breach of the IIA obligation to refrain from engaging in corruption, it may not become eligible for international protection under that IIA.35x Choudhury, above n. 1, at 91-2. These anti-corruption provisions can be found either within CSR clauses or in separate carve-out statements that exclude investments made through corrupt practices from the coverage of the investment protection provided by the IIAs.36x Y. Yan, ‘Anti-Corruption Provisions in International Investment Agreements: Investor Obligations, Sustainability Considerations, and Symmetric Balance’, 23 Journal of International Economic Law 989, at 990 (2020).

Civil/criminal liability: It is shown that liability exposure can stimulate responsible business practices.37x http://opiniojuris.org/2021/06/24/business-and-human-rights-symposium-mandatory-human-rights-due-diligence-and-civil-liability/ (last visited 5 December 2021). Some IIA provisions recognise investors’ civil and criminal liability for their actions that can, among others, affect individuals’ human rights enjoyment. These IIA provisions stipulate that investors may face civil liability claims made by individuals adversely affected by their investments and criminal penalties. These provisions can be considered as imposing an obligation of diligence on investors and may even be more than hortatory by prescribing consequences for investors’ certain failures.38x B. Choudhury, ‘Human Rights Provisions in International Investment Treaties and Investor-State Contracts’, SSRN Scholarly Paper, at 14 (2020).

Transparency: A group of IIA provisions oblige investors to provide information concerning their investments, corporate history and practices if requested by the states. Such disclosures may enable monitoring of the human rights record of foreign investments in a host state. Additionally, they may be instrumental in judicial cases where transnational enterprises are sued for their adverse human rights impacts but refuse to share information. It should be noted that transparency in investor-state dispute settlement (ISDS) is often used to refer to the procedural transparency of the dispute settlement proceedings. However, here it refers to the substantive treaty obligations of investors to disclose information to officials regarding their activities.

Corporate social responsibility: CSR is another topic found in many investor obligations provisions. Despite the absence of a universally agreed definition for CSR, the existing definitions often describe the concept consisting of five dimensions: stakeholder, social, economic, environmental and voluntariness.39x A. Dahlsrud, ‘How Corporate Social Responsibility is Defined: An Analysis of 37 Definitions’, 15 Corporate Social Responsibility and Environmental Management 1, at 6 (2008). Although CSR is a concept that originated from and for the business world, genuine adherence to CSR principles by business enterprises, including foreign investments, may positively influence the enjoyment of human rights.40x E. Giuliani, ‘Human Rights and Corporate Social Responsibility in Developing Countries’ Industrial Clusters’, 133 Journal of Business Ethics 39, at 45-6 (2016). In this regard, this group of investor obligations provisions may signal states’ commitment to promoting CSR principles and encouraging investors’ adherence to them.

Sustainable development: The concept of sustainable development consists of three dimensions: environmental, social and economic. Human rights are closely related to the environmental and social dimensions, and they are deeply interconnected with the achievement of sustainable development. In the context of IIAs, references to sustainable development appear in various places and formats. However, the context of these references varies, and, unlike CSR, it is not easy to interpret every reference to sustainable development as if it concerns investor behaviours. Instead, in some cases, such references demonstrate states’ commitment to sustainable development, and it can hardly impose any sort of obligation on investors.

Human rights: A significant group of IIA provisions refers to obligations for investors that occupy a central place in human rights law. They may prescribe obligations to protect the environment, human rights, labour rights or indigenous rights. These obligations are novel and rare in the states’ treaty practice. Advocates of balancing investment law through more investor obligations in IIAs often refer to provisions on these subjects and demand more of such obligations on investors.41x For instance, Dumberry argues that in a pragmatic sense, investor obligations aimed at balancing the asymmetries in future IIAs should be confined to those on human rights, labour rights, environment and anti-corruption. See: P. Dumberry, ‘Suggestions for Incorporating Human Rights Obligations into BITs’, in B. Ilge and K. Singh (eds.), Rethinking Bilateral Investment Treaties: Critical Issues and Policy Choices (2016) 211, at 216. For a case for more protection of third-party rights, including that of indigenous people, in IIAs, see: L. Cotula and N. M. Perrone, ‘Reforming Investor-State Dispute Settlement: What about Third-Party Rights?’, IIED Briefing Papers 2019, at 1-2 and J. Coleman and K. Cordes, ‘International Investment and the Rights of Indigenous Peoples’, CCSI Workshop Outcome Document 2016, at 5-12. These provisions can be grouped separately depending on the exact subject of the obligation. Alternatively, they may concern environmental protection (Environment), explicitly refer to human rights either by using the exact phrase or by referring to international human rights standards such as the UN Guiding Principles on Business and Human Rights (Human rights), refer to the protection of labour rights (Labour) or concern the rights of indigenous and local communities (Indigenous).

Asymmetrical structure: Lastly, some IIA provisions touch upon states’ and investors’ asymmetrical rights and obligations and the need for an overall balance. While at first glance these provisions do not concern human rights-related obligations for investors per se, a balancing exercise should include the introduction of such obligations into IIAs. Hence, provisions explicitly pointing out the substantive asymmetries in IIAs and the ISDS and striking a balance between states’ and foreign investors’ respective rights and obligations can be considered human rights-related. The following preambular statement exemplifies this category: ‘The Parties … securing an overall balance of rights and obligations between and among investors and host countries … hereby agree as follows…’42x Preamble Agreement between the Government of the Republic of South Africa and the Government of the Federal Democratic Republic of Ethiopia for the Promotion and Reciprocal Protection of Investments, 18 March 2008.

To conclude this section, an analysis of direct human rights obligations of investors alone would not be able to draw an accurate picture of the state of the art concerning investors’ human rights obligations in IIAs. Provisions on human rights-related investor obligations, as understood in this study, aim to regulate investor behaviours, and these behaviours can also have direct or indirect impacts on human rights enjoyment of foreign investment-affected individuals or groups of people. In this sense, the notion of human rights-related investor obligations encompasses not only direct human rights obligations on investors but also provisions concerning, for example, sustainable development, domestic law compliance, anti-corruption or civil liability of investors. -

3 Methodology

So far, legal scholars have pursued different approaches to investor obligations in the international investment regime. Three, in particular, stand out in the literature. One is to investigate a limited number of IIAs and categorise investor obligations based on different criteria such as whom they are addressed to or the topics they deal with.43x See e.g. K. Nowrot, ‘The Other Side of Rights in the Processes of Constitutionalizing International Investment Law: Addressing Investors’ Obligations as a New Regulatory Experiment’, 21 Rechtswissenschaftliche Beiträge der Hamburger Sozialökonomie Heft 1, at 12-20 (2018); Krajewski above n. 8. Another group of scholars adopt a more normative stance. They explore different ways in which investor obligations can be integrated into IIAs. They either adopt a more general perspective about the features of the regime and the necessity of integrating investor obligations44x See e.g. J. Gathii and S. Puig, ‘Introduction to the Symposium on Investor Responsibility: The Next Frontier in International Investment Law’, 113 American Journal of International Law 1 (2019); R. van Os and R. Knottnerus, ‘Investment Protection Agreements, Human Rights and Sustainable Development: An Uneasy Mix’, 59 Development 107 (2016). or focus on evaluating investor obligations on certain subjects such as environmental protection,45x See e.g. C. Baltag and Y. Dautaj, Investors, States, and Arbitrators in the Crosshairs of International Investment Law and Environmental Protection (2020). anti-corruption46x See e.g. Yan, above n. 36. or domestic law compliance.47x See e.g. R. Yotova, ‘Compliance with Domestic Law: An Implied Condition in Treaties Conferring Rights and Protections on Foreign Nationals and Their Property?’, University of Cambridge Faculty of Law Research Paper 2018:43. The last approach is to closely read a particular IIA, be it a model48x See e.g. E. Leikin, S. Gadodia & C. Loudon, ‘The State Doesn’t Strike Back After All: India’s Final Model BIT Takes the Bite out of Investor Obligations and Eliminates State Counterclaims’, 2 Transnational Dispute Management (2018). or a regular IIA,49x See e.g. O. Ejims, ‘The 2016 Morocco–Nigeria Bilateral Investment Treaty: More Practical Reality in Providing a Balanced Investment Treaty?’, 34 ICSID Review 62 (2019). or a selected arbitral award50x See e.g. L. Cotula, ‘Human Rights and Investor Obligations in Investor-State Arbitration: Hesham Talaat M. Al-Warraq v The Republic of Indonesia, UNCITRAL Arbitration, Final Award, 15 December 2014 (Bernardo M. Cremades, Michael Hwang, Fali S. Nariman)’, 17 The Journal of World Investment & Trade 148 (2016). to critically analyse formulation or interpretation of investor obligations included therein and argue for further improvement of the effectiveness of these provisions to balance the asymmetries of the regime.

Building on these approaches, this study takes a more ambitious approach to the issue of investor obligations in IIAs. First, it computationally identifies the provisions on investor obligations in all IIAs and then qualitatively evaluates them in terms of their impacts on the privileged position of foreign investors in the regime. A comprehensive picture of the problems with investor obligations in IIAs is drawn by following these steps. Thus, the method developed for this study provides an opportunity to delve further into the IIA universe and develop a deeper understanding of the investor obligations in IIAs than a manual approach. While this study does not claim to give the complete picture concerning the human rights-related investor obligations in IIAs, it is the most comprehensive on this subject to date.3.1 Dataset

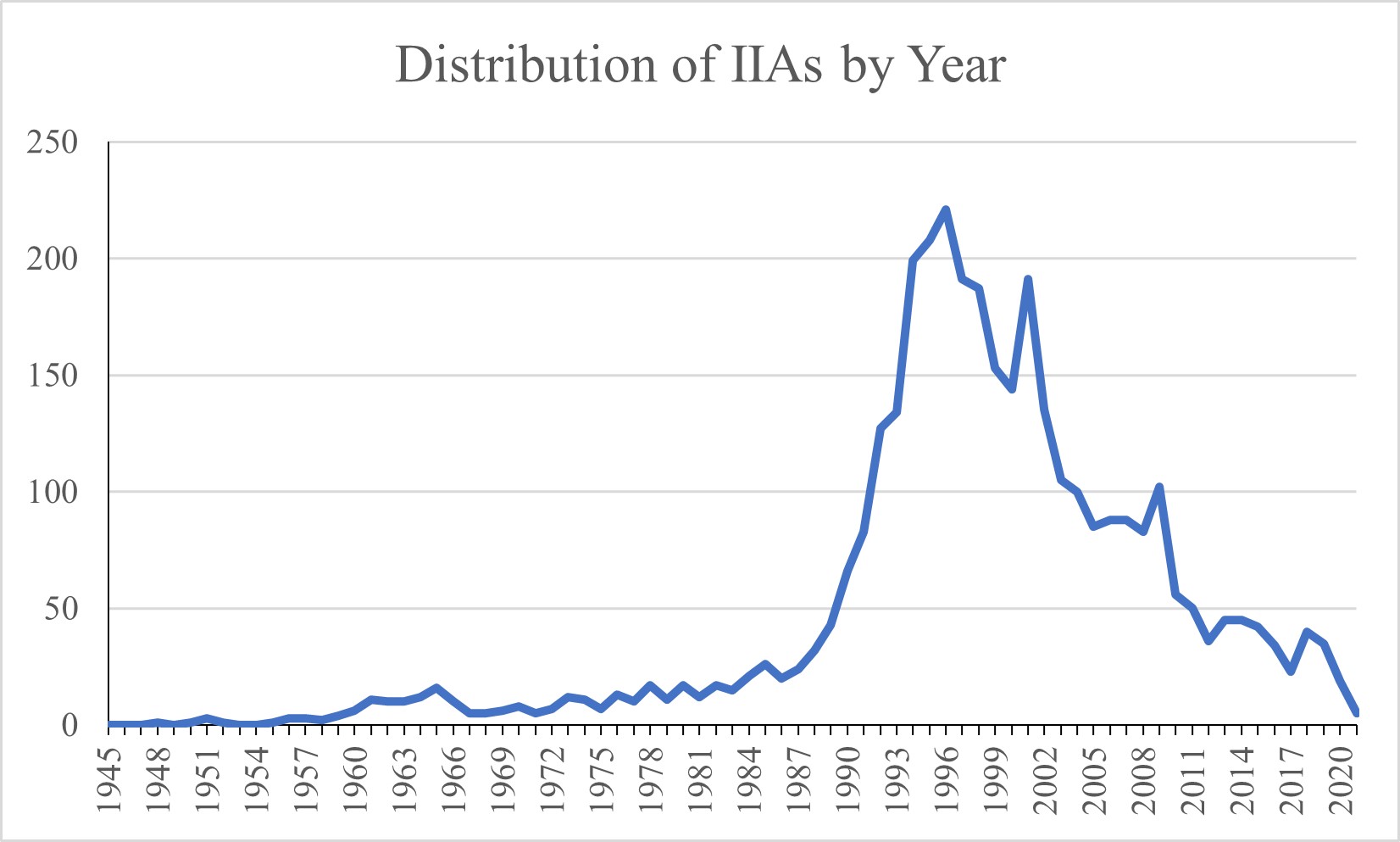

For the purposes of this study, I conducted an automated textual analysis on 3,558 publicly available IIAs.51x This number consists of all the available IIAs on EDIT database as of 18 November 2021. Model IIAs are not included in the analysis. These IIAs were retrieved from the Electronic Database of Investment Treaties (EDIT).52x W. Alschner, M. Elsig & R. Polanco, ‘Introducing the Electronic Database of Investment Treaties (EDIT): The Genesis of a New Database and Its Use’, 20 World Trade Review 73 (2021). This database consists of all the publicly available IIAs. What distinguishes this database from others on investment agreements is that on EDIT, agreements concluded in different languages are translated into English, either automatically or by contributors, so that all the IIAs can be downloaded in one language (Figure 1).

Distribution of IIAs by Year

Among the 3,558 IIAs, 426 are treaties with investment provisions (TIPs). This category is broad. For instance, the Treaty on European Union; economic partnership agreements; and bilateral, multilateral or regional free trade agreements (FTAs) are in this category. The remaining 3,132 IIAs are BITs. The data set spans the period 1948 to 2021.

3.2 Research Design

The research design consisted of two steps. In the first step, in order to identify IIA provisions on investor obligations, I employed automated textual analysis that uses machine-coding based on dictionaries consisting of words, phrases and word sequences. I devised these dictionaries after studying a large number of IIAs and scholarly publications and used them to identify and locate where each of the dictionary entries is found in the corpus of IIAs. The entries were created based on the use of common words and phrases in relevant investor obligations provisions that were manually found in different IIAs. In the second step, I surveyed all the provisions identified in the first step to classify them along the five dimensions. For each provision, I determined the year the IIA containing that provision was concluded, whether it is in the main text or preamble of the IIA, whether it is addressed to states or foreign investors, whether it is mandatory or voluntary on investors and what the subject of obligation is.

In the first step, I devised three different dictionaries with different purposes. The first dictionary aimed to identify potentially relevant provisions for the purposes of this study and consisted of elements common in provisions on investor obligations.53x For instance, the first dictionary is used to find provisions where the words ‘investor’ or ‘investment’ appear before verbs such as ‘shall’, ‘should’ or ‘must’ or phrases like ‘corporate social responsibility’, ‘socially responsible’ or ‘tax/fiscal obligations’. This dictionary was intentionally kept long and included elements that yielded more irrelevant results than relevant ones. The objective was to identify the maximum number of potentially relevant provisions. The second dictionary aimed to remove the irrelevant results to the largest extent possible. It consisted of words and phrases that were highly unlikely to be found in human rights-related investor obligations provisions.54x The computational analysis based on the first dictionary yielded many irrelevant results. For instance, provisions containing ‘investors shall have the right to …’ have also been identified. To remove such provisions, the second dictionary consisted of words and phrases like ‘fair and equitable’, ‘expropriation’, “investment environment’ or ‘full protection’ as these are very unlikely to be used in the context of human rights-related investor obligations. This was a necessary step since there were thousands of provisions after the first search, most of which were irrelevant for this study and had to be removed. However, after this second step, some provisions that were relevant have also been unintentionally removed. For instance, some treaty preambles or long provisions that deal with different issues could contain elements from both the first and the second dictionaries. In such cases, they were removed after conducting the search by using the second dictionary. In this light, the third dictionary aimed to identify relevant provisions unintentionally removed in the previous step. It consisted of elements related to specific human rights-related subjects found in IIAs, such as corruption, taxation or protection of the environment, human rights and labour rights.55x For instance, the third dictionary consisted of words and phrases like ‘human rights’, ‘labour rights’, ‘sustainable development’ or ‘in accordance with laws and regulations’.

The dictionaries were created on the basis of the study of the relevant literature and the examination of a large sample of IIAs in search of investor obligations provisions to identify words, phrases or word patterns to be included in the dictionaries. To triangulate my findings from the literature and IIAs, the dictionaries were devised in consultation with colleagues with expertise in the subject matter. Although the dictionaries were kept as comprehensive as possible to make up for minor differences in the use of language from one IIA to another, it was impossible to be entirely sure that all such different language uses were included in the dictionaries without going through all the IIAs manually, rendering the automated textual analysis pointless. Before finalising the dictionaries, trial runs with varying numbers of random IIAs have been conducted to identify as many subtle differences as possible in the relevant provisions and use of similar words and phrases that convey the same meaning.

After the computational quantitative analysis to collect the relevant IIA provisions, these provisions were manually classified based on the five dimensions to assess their potential to effectively address the issue of (absence of) investor obligations in IIAs and the resulting substantive asymmetries. In this step, one by one, all provisions identified in the automated textual analysis were classified according to the five aforementioned dimensions. If an article dealt with multiple subjects, such a provision was counted as many as the number of subjects so that all these different subjects could be reported. This qualitative step was necessary to complement the quantitative results, give them more meaning and mitigate some of the shortcomings of computational analysis.56x For instance, in such a research design, the software cannot understand the context in which the words it encounters are used or the significance of those words in their own context. Also, it misses the meaning of the provisions containing these words. It just identifies the provisions containing the words from the dictionaries. The interpretation of these provisions is on the researcher. Thus, legal hermeneutics are essential in such a research design. It is noted that ‘quantitative methods should be viewed as complementary to and not in competition with the traditional hermeneutic approach to law’. See T. Altwicker, ‘International Legal Scholarship and the Challenge of Digitalization’, 18 Chinese Journal of International Law 217 (2019). For a general overview on the shortcomings of the use of automated textual analysis in legal and political texts, see: Text as Data: J. Grimmer and B. M. Stewart, ‘The Promise and Pitfalls of Automatic Content Analysis Methods for Political Texts’, 21 Political Analysis 267 (2013).

The dimensions of the taxonomy devised for this study to analyse human rights-related investor obligations are as follows:3.2.1 Year

The literature often observes that the number of human rights-related investor obligations provisions is increasing. However, it begs for further elaboration on how the states’ approach to these provisions changes and to what extent they incorporate them into their IIAs concluded in different years. Knowing that, on average, how many such provisions can be found in an IIA enables quantification of this change and, therefore, provides a clearer picture of the trends among states in incorporating human rights-related investor obligations into their IIAs.

3.2.2 Location in Treaty Text

Provisions on investor obligations in an IIA can be found in either preamble or body, including annexes. Preambles in international agreements can serve a variety of functions. Only in infrequent circumstances can they impose obligations on the parties.57x M.M. Mbengue, ‘Preamble’, Max Planck Encyclopaedias of International Law 2006, at paras. 12-4. In the context of investment law, preambles certainly do not impose obligations. Tribunals often rely on preambles for interpretative purposes only and to discern between the rights and obligations of treaty parties, i.e. states, but not those of investors.58x M.H. Hulme, ‘Preambles in Treaty Interpretation’, 164 University of Pennsylvania Law Review 1281, at 1320 (2016). They are not considered among the operational sections of an IIA and ‘refer to a wide range of non-economic policy objectives only in the vaguest terms’.59x S.A. Spears, ‘The Quest for Policy Space in a New Generation of International Investment Agreements’ 13 Journal of International Economic Law 1037, at 1071 (2010). Thus, even though there are preambles containing references to investor obligations, the effect of these preambles on balancing the substantive asymmetries within the international investment regime is severely limited.60x The award in the Eco Oro v. Colombia case is illustrative of the arbitrators’ exercise of preamble interpretation and balancing of different, and even occasionally conflicting, objects and purposes of an IIA. Even after noting that environmental protection and investment protection are among the objects and purposes of the Canada-Colombia FTA and none is subservient to the other, the Tribunal ordered payment of compensation to the investor, thereby effectively ignoring investor’s accountability for its environmental damages. See: ICSID, Eco Oro Minerals Corp. v. Republic of Colombia, Decision on Jurisdiction, Liability and Directions on Quantum, 9 September 2021. See also: www.cckn.net/itn/es/2021/12/20/eco-oro-and-the-twilight-of-policy-exceptionalism/ (last visited 24 May 2022).

To stipulate obligations on investors in an IIA, the difference between a provision in the preamble and in the body is essential. As is the case almost in every international agreement, the body part of an IIA is where the rights and obligations of the parties and relevant stakeholders are prescribed. Provisions in the main text can give the parties the right to have claims. Therefore, ceteris paribus, whether a provision on investor obligations is located in the preamble or the body of an IIA is a key determinant when assessing the potential of that provision to strike a balance between the respective rights and obligations of foreign investors and other stakeholders in the regime. While the provisions found in an IIA preamble were classified as preamble, the ones located in the main text of IIAs were classified as body.3.2.3 Addressee of the Provision

Investor obligations in IIAs either directly impose obligations on investors or are addressed to the state and require them to regulate investor activities. As to the latter type of obligations, if states fail to carry out these obligations prescribed, there may be nothing leading investors to change their behaviours. However, if the states fulfil these obligations, they can indirectly oblige investors to act in prescribed ways. The following provision is illustrative of this group of provisions: ‘Each Party shall strive to promote compliance with its environmental guidelines by enterprises operating in its territory.’61x Art. 197 Free Trade Agreement between the Republic of Korea and the Republic of Peru, 14 November 2010. It is clear that investors may face new obligations if the state parties comply with this provision. These provisions are categorised as indirect.

On the other hand, increasingly, more IIA provisions are addressed directly to investors. Unlike the provisions addressed to states, these provisions do not require a state action prior to creating an obligation on investors. Thus, they can be more capable of necessitating investors to act in a particular manner or refrain from prescribed activities. These provisions, classified as direct, may serve a better balancing function than the indirect provisions. An example is the following: ‘Investors and investments should apply national, and internationally accepted, standards of corporate governance for the sector involved, in particular for transparency and accounting practices.’62x Art. 10(3) Agreement between the Slovak Republic and the Islamic Republic of Iran for the Promotion and Reciprocal Protection of Investments, 19 January 2016.3.2.4 Strictness of the Provision’s Language

As for the strictness of the language in human rights-related obligations on investors, there are two main categories: hortatory/aspirational and mandatory.

The hortatory/aspirational category covers a broad spectrum of provisions. For instance, preambular provisions on investors’ obligations fall in this category. Provisions in this category do not lay down clear and actionable duties for investors. Rather, they may encourage investors to take specific actions or adhere to certain standards throughout their investment-related activities. They may also encourage or require investors to direct their best efforts to achieving higher human rights-related standards in their operations. The following examples illustrate well the characteristics of these provisions in this category: ‘The Parties shall encourage cooperation between enterprises in relation to goods, services and technologies that contribute to sustainable development and are beneficial to the environment’63x Art. 39(4) Free Trade Agreement between the EFTA States and Bosnia and Herzegovina, 24 June 2013. or ‘Investors and their investments will strive to achieve the highest possible level of contribution to the sustainable development of the Host State Party and the local community, through the adoption of a high degree of socially responsible practices, based on the principles and voluntary standards established in this Article’.64x Art. 14(1) Intra-MERCOSUR Cooperation and Facilitation Investment Protocol, 7 April 2017.

Despite some variations, the use of language in these provisions necessitates putting them in one category. These provisions often use imprecise and soft language, which renders them non-justiciable. As a result, even though these provisions still concern investors’ actions, they are unlikely to increase investors’ respect for human rights in their host states on their own and demonstrate a limited potential to oblige investors to act in a particular manner. It is also practical to gather these provisions in one major category. The differences between these provisions in language strictness and justiciability are hardly distinguishable in many cases.

Mandatory provisions on investor obligations prescribe duties on investors through modal verbs like shall or must. These provisions have the most significant potential to serve as a ground, for instance, for states to bring forth counterclaims in an investment dispute if they have the right to do so. Consequently, if investors fail to fulfil these obligations, this can affect the tribunal’s determination of jurisdiction, liability or the calculation of the damages to the investor’s disadvantage.65x For instance, if a tribunal decides that a claimant has violated its human rights-related obligations, depending on the specifics of the underlying IIA and the case, it may alternatively decide that it lacks jurisdiction to decide on the dispute; the case is inadmissible; the investor has a liability in the dispute; or a lower amount of compensation than that claimed. For a more detailed explanation on this, see: F. Balcerzak, ‘Jurisdiction of Tribunals in Investor–State Arbitration and the Issue of Human Rights’, 29 ICSID Review 216, at 218 (2014). Thus, regardless of certain procedural hurdles, these provisions seem to be the most promising in balancing the substantive asymmetries between the rights and obligations of all stakeholders. The following provision illustrates this type of provisions: ‘Investors of a Party and its investments shall not offer, promise or grant any monetary advantage … to obtain undue advantages.’66x Art. 8.16(2) Trade Agreement between the Argentine Republic and the Republic of Chile, 2 November 2017.3.2.5 Subject Matter of the Obligation

Human rights-related investor obligations may touch on a variety of subjects that were explained in the preceding section in detail. Therefore, I confine myself to only naming them here: investor/investment definition conditioning domestic law compliance; domestic law compliance; tax/fiscal obligations; corporate governance; anti-corruption; civil/criminal liability; transparency; CSR; sustainable development; human rights; asymmetrical structure. Although the subject matter alone cannot tell much about the enforceability of an obligation, analysing it may provide valuable insights concerning the past and current trends about investor obligations in IIAs.

All these categories under various dimensions correspond to different degrees of stringency of obligations on investors. Regardless of the substance of an obligation, a provision is highly stringent if it is located in the main text of an IIA (body), addressed to investors (investor) and formulated in a more binding manner (mandatory). This means that provided that relevant procedural conditions, e.g. the possibility of raising counterclaims, are also met, such provisions can lead to enforceable obligations on investors in an ISDS case. Consequently, investors can be held accountable by an arbitral tribunal for their breaches of these obligations. It should be noted that the subject matter of an obligation is not a valid indicator of stringency. Whether an obligation is about, say, combating corruption or protecting human rights does not say anything regarding the bindingness of the obligation. In this light, Table 1 illustrates which categories denote more or less stringent obligations on investors.Table 1 Dimensions and the Degree of StringencyMore stringent obligations Less stringent obligations Location

Body

Location

Preamble

Addressee

Investor

Addressee

State(s)

Language

Mandatory

Language

Hortatory/aspirational

-

4 Evolution of Investor Obligations – Turning Tides?

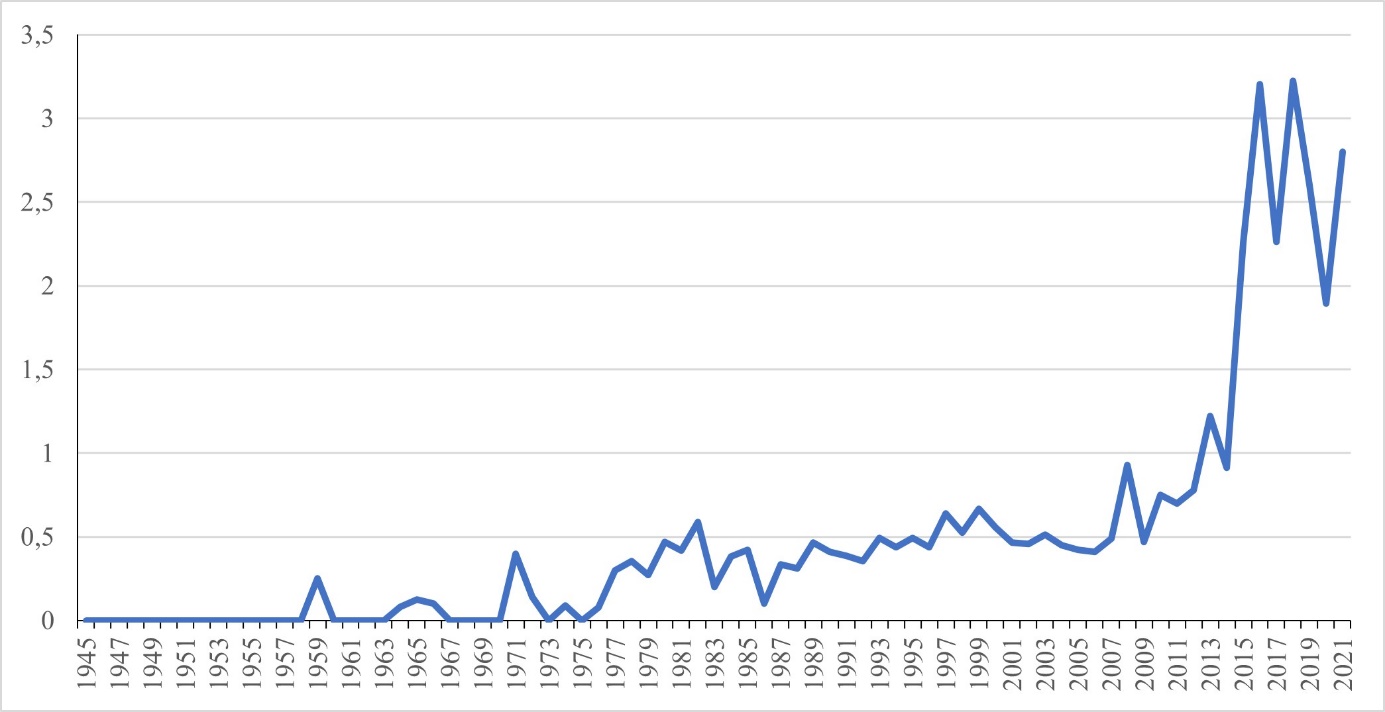

Average Number of Provisions on Investor Obligations per IIA

The results of the computational analysis partly corroborate existing findings in the literature on investor obligations. They also reveal certain unexplored features of these provisions and IIAs. After the computational analysis, 2,183 provisions on investor obligations were identified in 1,236 IIAs out of 3,558. This means that almost one-third of all the IIAs concluded since 1948 contain at least one provision on investor obligations. Figure 2 indicates the average number of investor obligations provisions in the IIAs concluded in a given year. Despite some fluctuations in the average number of such provisions, there has been an upward trend since the first IIAs. The increase in these provisions accelerated drastically around 2013. Whereas, on average, there are three provisions on investor obligations in an IIA concluded in 2018, this average was less than one during the entire period before 2013. In the future, it can be expected that this average will continue to increase, as the trend shows.

These results are in line with the findings in the literature that observe this shift in IIA drafting concerning investors’ obligations. By quantifying this increase and detailing the number of these provisions, this study offers a thicker and more accurate description of this trend. There can be various reasons for the dramatic increase in the 2010s. For instance, this trend shift coincides with the mandate of Prof. John Ruggie, Special Representative of the UN Secretary-General on the issue of human rights and transnational corporations and other business enterprises and the strengthening of the understanding that private entities should bear international responsibility for their adverse impacts.67x CHR Res. E/CN.4/RES/2005/69, 20 April 2005. Translated into the context of investment law, this understanding can appear in the form of human rights-related obligations for investors. Another potential explanation for this trend shift could be the increased levels of public scrutiny and scepticism over IIAs and their impacts on public interests in social, environmental and health issues, as well as on state sovereignty.68x T. Fritz, International Investment Agreements Under Scrutiny: Bilateral Investment Treaties, EU Investment Policy and International Development (2015), at 5. Coupled with the ever-increasing flow of capital worldwide and several highly publicised foreign investment-related human rights disasters,69x www.business-humanrights.org/en/from-us/lawsuits-database/ (last visited 05 December 2021) (hereinafter Lawsuits Database).Table 2 Number of Relevant Provisions in Each IIA1 ECOWAS Supplementary Act on Investments (2008) 28 In force 2 Morocco – Nigeria BIT (2016) 26 Not entered into force 3 Intra-MERCOSUR Investment Facilitation Protocol (2017) 17 In force 4 Brazil – Morocco BIT (2019) 16 Not entered into force 5 Brazil – Chile FTA (2018) 15 Not entered into force 6 Brazil – Guyana BIT (2018) 14 Not entered into force 7 Brazil – India BIT (2020) 14 Not entered into force 8 Brazil – Suriname BIT (2018) 14 Not entered into force 9 Brazil – United Arab Emirates BIT (2019) 14 Not entered into force 10 China – EU Comprehensive Agreement on Investment (2021) 13 Not entered into force 11 Brazil – Malawi BIT (2015) 12 Not entered into force 12 Iran – Slovakia BIT (2016) 12 In force 13 Brazil – Ecuador BIT (2019) 11 Not entered into force 14 Brazil – Ethiopia BIT (2018) 11 Not entered into force 15 Brazil – Mexico CFIA (2015) 11 In force 16 Brazil – Mozambique CFIA (2015) 11 Not entered into force 17 Angola – Brazil CFIA (2015) 10 In force 18 Brazil – Colombia CFIA (2015) 10 Not entered into force 19 EFTA – Costa Rica – Panama FTA (2013) 9 Not entered into force 20 Hungary – Kyrgyzstan BIT (2020) 9 Not entered into force 21 Argentina – UAE BIT (2018) 8 Not entered into force 22 Belarus – Hungary BIT (2019) 8 In force 23 Bosnia and Herzegovina – EFTA FTA (2013) 8 In force 24 Brazil – Chile CFIA (2015) 8 Not entered into force 25 Cape Verde – Hungary BIT (2019) 8 Not entered into force this public scrutiny might have led states to manage and mitigate a public backlash by attempting to regulate foreign investor behaviour via drafting more balanced IIAs.

While 1,236 IIAs contain relevant provisions, 902 of them are currently in force. The remaining IIAs were either terminated or did not enter into force for various reasons. More than half of these IIAs with investor obligations provisions contain only one such provision, and only eighteen IIAs contain ten or more (0.51% of the entire sample) (Table 2). All eighteen of these IIAs were concluded since 2008, and an overwhelming majority of these are the new-generation Brazilian IIAs. Strikingly, only five of these IIAs (0.14% of the entire sample) have entered into force. The remaining IIAs are still pending ratification and entry into force. It is not surprising that the ECOWAS Supplementary Act on Investments (2008) and Morocco – Nigeria BIT (2016) (though still not in force) are on top of this list. The ECOWAS Supplementary Act has been hailed in the literature as an exemplary IIA in terms of formulation of investor obligations70x L. Cotula, ‘Raising the Bar on Responsible Investment: What Role for Investment Treaties?’, IIED Briefing Papers 2018, at 3. from which the Morocco – Nigeria BIT has taken much of its inspiration. The fact that these two IIAs appear on top of the list can be taken to verify the validity of the dictionaries created for this study. It is also striking that only in one IIA in this list, capital-exporting developed states can be found as a party (i.e. China – EU Comprehensive Agreement on Investment (2021)), and this IIA remains not in force. Hence, out of the entire sample, there is not even one IIA that (a) contains ten or more human rights-related provisions on investors, (b) has capital-exporting developed states as parties and (c) has already entered into force. This raises the question of whether this trend is followed by a large group of states and can eventually result in a change in the asymmetrical structure of the international investment law regime.

Looking at the parties to the IIAs with the most frequent human rights-related investor obligations provisions, it appears that this trend does not resonate with the majority of states, especially developed and capital-exporting states. Instead, a few states continue this trend more strongly. These are primarily capital-importing developing states that have suffered from investor claims targeting their legitimate public policies71x See e.g. ICSID, Piero Foresti et al. v. Republic of South Africa, Award, 4 August 2010. or where transnational business enterprises committed grave human rights abuses in the past, such as Ecuador and Nigeria.72x For instance, for an overview of lawsuits against multinational companies for their human rights violations in their host states, see: Lawsuits Database, above n. 69. Even if these states have a very long way ahead too, few of the pioneer states, such as Brazil (it should be noted that there is no ISDS in Brazilian BITs in force) and some African states are taking the lead in concluding less asymmetrical IIAs. On the issue of investor obligations, these states seem to move towards being rule-makers in terms of imposing obligations on investors in their IIAs.73x For an overall assessment of rule-takers and rule-makers in investment law system, see: Alschner and Skougarevskiy, above n. 9. At its origin, the sole focus of the investment regime on investor protection and its disregard for the public welfare of the capital-importing host state were clear reflections of the colonial and imperialist roots of the regime aimed at protecting the interests of capital-exporting states.74x K. Miles, The Origins of International Investment Law: Empire, Environment and the Safeguarding of Capital (2013), at 2-3. However, inserting more provisions on investor obligations by certain, albeit few, developing states marks an attempt to depart from the exploitative origins of the international investment law regime.

However, as long as developed states that regulate considerably larger proportions of global investment flows do not adhere to this phenomenon, this departure imprinted by a few developing states cannot be as influential in revising some of the exploitative fundamentals of the international investment law regime. At best, it can be stated that, so far, developed states have concluded some IIAs containing slightly more provisions on investor obligations than their traditional IIAs. However, such IIAs are exceptional in the IIA stock of developed states. These exceptions verify the general trend among these states that they are not very much in favour of drafting IIAs that can balance the inherent asymmetries in the investment law regime.

Interestingly, states that have been historically active in concluding IIAs and forerunners in prescribing human rights obligations for private enterprises do not show a noticeable appetite to conclude more balanced IIAs. For instance, developed states like France, Germany, the UK and the Netherlands have long been prominent actors in concluding IIAs.75x https://investmentpolicy.unctad.org/international-investment-agreements/by-economy (last visited 5 December 2021). These countries have also enacted legislation or taken various initiatives to regulate extraterritorial activities of business enterprises headquartered or domiciled in their jurisdictions to prevent them from being complicit or linked to human rights abuses abroad.76x https://knowledgeproducts.nortonrosefulbright.com/nrf/business-and-human-rights-around-the-world (last visited 5 December 2021 and www.business-humanrights.org/en/latest-news/database-supply-chain-due-diligence-laws-regulations-agreements-initiatives/ (last visited 5 December 2021). Yet, despite this legislative activism, the results show that they prefer to avoid relying on investment law for that purpose. It appears that the reluctance of these states to draft more human rights-related investor obligations provisions in their IIAs results from political choices rather than legal concerns.77x Van der Ploeg, above n. 14, at 115. They apparently do not want to subject their investors’ actions to the scrutiny of arbitrators or other foreign adjudicators. This means that even though by concluding IIAs every state renounces part of their sovereignty, developed capital-exporting states still do not want to expand this renouncement to their investors’ disadvantage, thereby exploiting the colonial origins of the international investment law. There seems to be a considerable degree of path dependency at play here.

However, it could be argued that instead of the number of provisions, how they are formulated is a more critical factor. Even treaties containing one single investor obligation provision may be more impactful than treaties with more than one. Therefore, in the next section, it is necessary to unpack the substantive content of these provisions and offer an in-depth analysis of their evolution and significance. -

5 Quality versus Quantity? Analysing Human Rights-related Investor Obligations

After the automated textual analysis, the outcome of the taxonomy gets even more insightful and exciting. A total of 2,183 investor obligations provisions identified in the quantitative analysis may seem higher than many scholars estimate. However, the picture does not seem promising when each of these provisions is classified based on the five aforementioned dimensions.

Table 3 Distribution of the Provisions based on Location, Addressee and Strictness of the LanguageDirect Indirect Grand Total Body 319 1676 1995 Hortatory/aspirational 179 161 340 Mandatory 140 1515 1655 Preamble 188 188 Hortatory/aspirational 188 188 Grand total 319 1864 2183 Table 3 indicates the distribution of the provisions based on their location, addressee and language. As for the language, an overwhelming majority of these provisions employ a strict language and stipulate mandatory rules. Additionally, more than 90% of these provisions (1995 out of 2,183) are located in the body sections of the IIAs. However, more than 85% of these provisions (1864 out of 2,183) are not directly addressed to investors but, instead, are directed to states as duty-bearers. States assume the duty of imposing obligations on investors, but investors are not put under any direct burden in most cases.

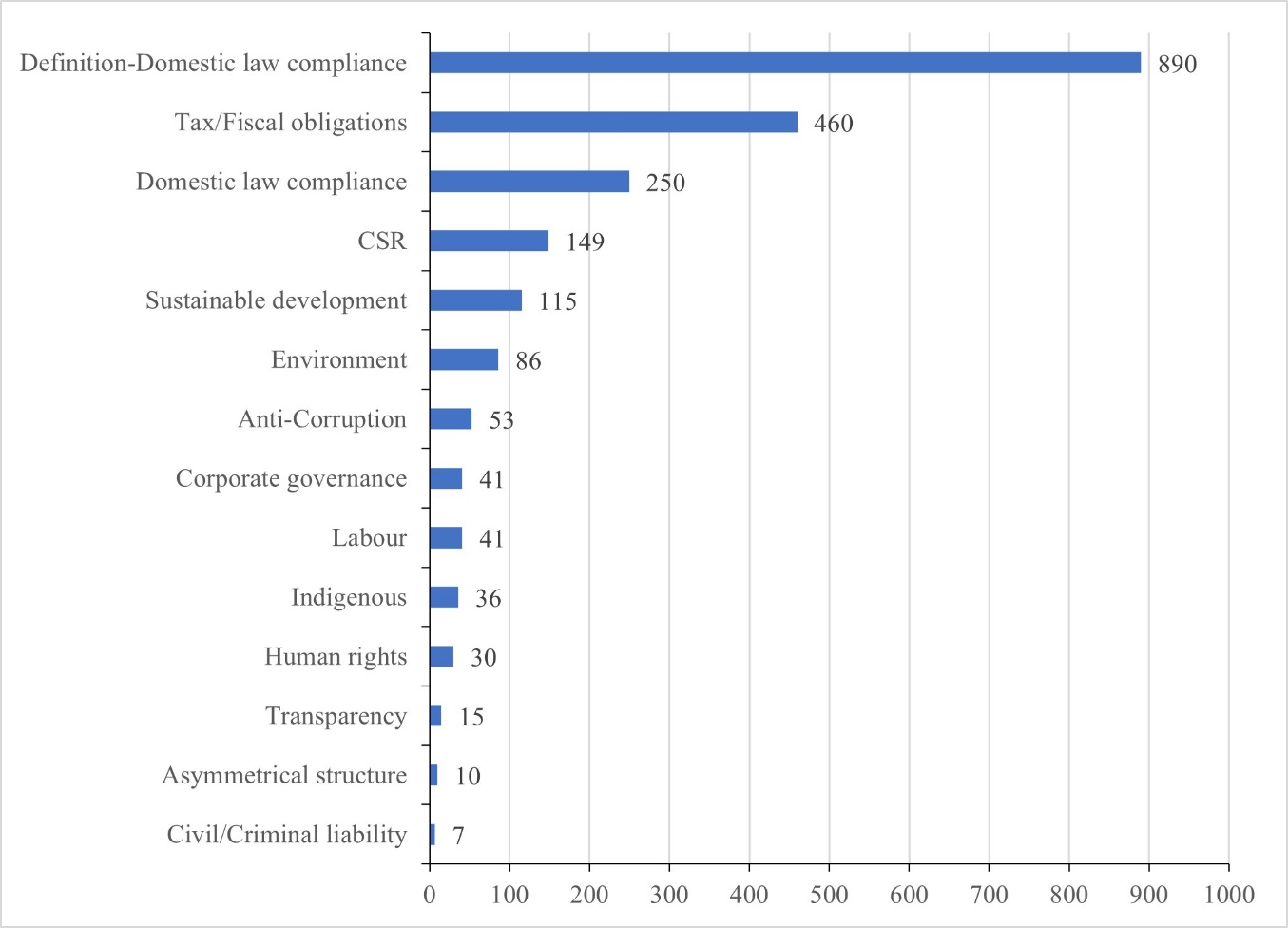

Number of Provisions by Their Subject

Breaking down these provisions according to their substance (Figure 3), it must be noted that around three-quarters of these provisions stipulate that investors should comply with their host state’s legislation and rules on taxation and fiscal obligations. Moreover, most of the compliance provisions refer to pre-establishment obligations for investors and investments, and only some stipulate post-establishment obligations. Additionally, compliance with tax and fiscal obligations provisions overwhelmingly refer to these obligations abstractly and in the context of the transfer of funds abroad. They stipulate that transfer of funds is possible only if these tax and fiscal obligations have been fulfilled, but they do not deal explicitly with issues like tax evasion or tax avoidance.

The large share of compliance with domestic laws and tax and fiscal obligations provisions in the results necessitates further consideration. On the one hand, this phenomenon indicates that states generally have the understanding that to be eligible for the protections afforded by IIAs, investors are required to comply with their national laws during, and in rare cases after, the admission and establishment of their investments.78x Yotova, above n. 47, at 14-5. Even if such a provision is absent in an IIA, most investment tribunals acknowledge that legality is an impliedNumber of Provisions on Different Subjects

requirement for investments, and treaty protections should not be extended to investments tainted with corrupt or fraudulent behaviours.79x Ibid., at 23.

On the other hand, it is strange that such provisions are thought to be necessary by states and inserted into IIAs in the first place. These provisions may indeed serve to internationalise investors’ duty of compliance with domestic laws. However, any natural or legal person in a foreign state should comply with that state’s laws and regulations, especially with those that can entail civil and criminal liability. Moreover, despite still being a contentious matter,80x K.P. Sauvant and G. Ünüvar, ‘Can Host Countries Have Legitimate Expectations?’, SSRN Scholarly Paper, at 2 (2016). reversing the question of investors’ legitimate expectations, it is argued that host states can also have the legitimate expectation that foreign investors will comply with their domestic laws and regulations.81x A. Bjorklund, ‘Improving the International Investment Law and Policy System: Report of the Rapporteur Second Columbia International Investment Conference: What’s Next in International Investment Law and Policy?’, in J.E. Alvarez and K.P. Sauvant (eds.), The Evolving International Investment Regime: Expectations, Realities, Options (2011), at 229. This is the case even if an IIA does not explicitly incorporate domestic laws on human rights into these compliance provisions.82x See e.g. Art. 7(1) Netherlands Model Investment Agreement, 22 March 2019. Since, in theory, domestic laws can encompass domestic human rights laws, such a reference would be devoid of any added value.83x Krajewski, above n. 8, at 120.

However, the application of these provisions falls considerably short of what they are theoretically capable of in terms of imposing human rights-related obligations on investors. First, when states claimed that they could legitimately expect foreign investors to respect their domestic regulatory frameworks, these invocations did not have a noticeable effect on the final award.84x Sauvant and Ünüvar, above n. 80. Moreover, arbitral tribunals have not faced the question of whether these compliance provisions also cover human rights laws. Other than the ones about corruption, human rights-related obligations of investors have not been a matter of concern for tribunals when interpreting these provisions. Hence, even though the compliance provisions constitute the largest share of human rights-related provisions on investor obligations, in practice, they have not been successfully employed to hold investors accountable for most of their adverse human rights impacts in their host states so far.

Similar points can also be raised concerning the tax and fiscal obligations provisions. These provisions often do not mention the duty of refraining from tax evasion and tax avoidance, which can generate severe human rights issues with potentially extensive adverse public economic and social impacts.85x M.J. Freire-Serén and J.P. Martí, ‘Tax Avoidance, Human Capital Accumulation and Economic Growth’, 30 Economic Modelling 22, at 29 (2013). Arguably the only consequence foreign investors may face in case of non-fulfilment of these obligations is that they may not be allowed to transfer funds abroad. In this case, just preventing investors from transferring their funds abroad seems like an inadequate and disproportionate measure to a breach of obligation with potentially grave public consequences.

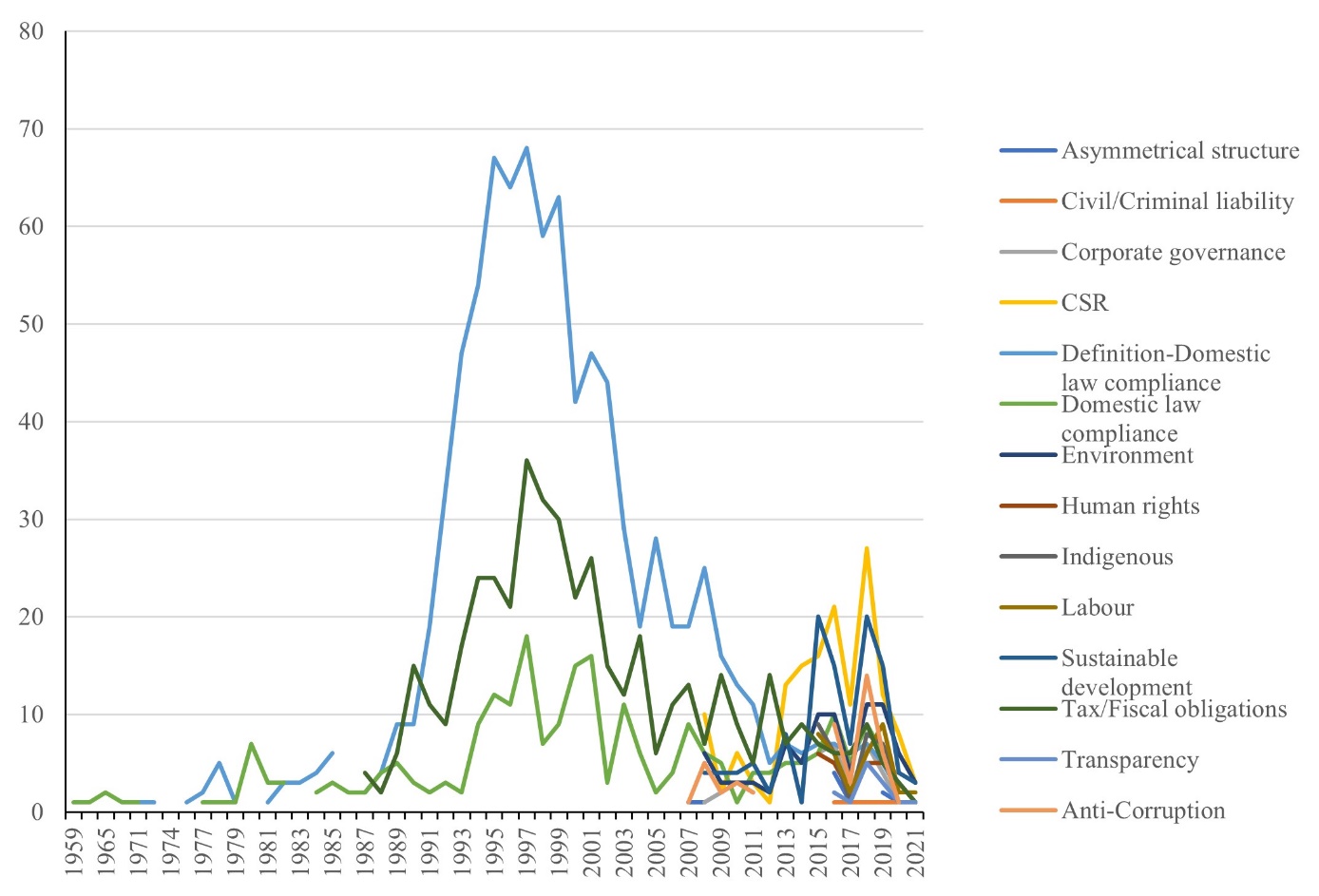

As for the distribution of different obligations per year (Figure 4), until around 2008, only a few types of obligations could be found prominently in IIAs, and these were compliance with domestic laws and fulfilment of tax and fiscal obligations. Especially during the IIA boom in the 1990s, these obligations have appeared frequently in IIAs. However, this picture has changed sinceTable 4 Strictness of the Language of Provisions on Certain SubjectsHortatory/Aspirational Mandatory Grand Total Asymmetrical structure 9 1 10 Civil/criminal liability 4 3 7 Corporate governance 39 2 41 CSR 145 4 149 Sustainable development 112 3 115 Transparency 4 11 15 Anti-corruption 24 29 53 Environment 68 18 86 Human rights 25 5 30 Indigenous 31 5 36 Labour 31 10 41 Grand Total 492 91 583 Table 5 Locations of Provisions on Certain SubjectsBody Preamble Grand Total Asymmetrical structure 2 8 10 Civil/criminal liability 7 7 Corporate governance 24 17 41 CSR 113 36 149 Sustainable development 62 53 115 Transparency 14 1 15 Anti-corruption 36 17 53 Environment 75 11 86 Human rights 26 4 30 Indigenous 36 36 Labour 32 9 41 Grand Total 427 156 583 around 2008. Specifically, obligations on newer subjects concerning, for example, CSR, sustainable development or environmental protection have started to make their way into IIAs and have even attained a more significant proportion in the entire list of provisions on human rights-related investor obligations. Also in this period, the subjects of obligations have diversified, and various subjects that were previously non-existent in IIAs started to be dealt with more commonly, such as anti-corruption, corporate governance and labour and human rights protection.

Explanations brought forward in the previous section for the trend shift in the 2010s, such as the emergence of new discourses regarding the place of private enterprises in international law and the public scrutiny over IIA negotiations, could also be valid for the change of subjects of investor obligations throughout the observed period and their diversification. As for the increase in the share of obligations on CSR and sustainable development, it should first be noted that these are not binding legal doctrines per se, and their respective definitions and scopes are not clear. This lack of clarity can seriously complicate the enforceability of a legal obligation. With their focus on and encouragement ofTable 6 Addressee of Provisions on Certain SubjectsDirect Indirect Grand Total Asymmetrical structure 10 10 Civil/criminal liability 4 3 7 Corporate governance 22 19 41 CSR 41 108 149 Sustainable development 37 78 115 Transparency 14 1 15 Anti-corruption 18 35 53 Environment 32 54 86 Human rights 21 9 30 Indigenous 33 3 36 Labour 25 16 41 Grand Total 247 336 583 voluntarism,86x A. Ramasastry, ‘Corporate Social Responsibility Versus Business and Human Rights: Bridging the Gap Between Responsibility and Accountability’, 14 Journal of Human Rights 237, at 252 (2015). these obligations may be considered a middle ground between placing no responsibility on foreign investors and recognising their responsibilities for less ambiguous obligations such as the ones concerning environmental, human rights and labour rights protection. Yet one downside of this approach is that provisions on CSR or sustainable development are not very helpful in establishing definitive obligations on investors owing to the lack of clarity of their exact scope.

Very few of these identified IIA provisions touch on subjects like sustainable development, human rights or the environment (Table 4, 5, 6). It is frequently stressed in the literature that provisions dealing with these subjects are largely absent in IIAs, and this has been pointed out as one of the major shortcomings of IIAs.87x See e.g.: Choudhury, above n. 38, at 10-11. The results of the analysis verify this absence as well. Even though such provisions are on the rise, out of the 2,183 provisions on investor obligations, only 583 of them (about 27%) deal with such subjects.

These modern provisions occupy different positions across the soft-hard law spectrum for the rules on regulation of business conduct with human rights impacts. On the soft law end, there are provisions that, for example, state that ‘investors … should make efforts to voluntarily incorporate internationally recognised standards of corporate social responsibility into their business policies and practices’.88x Art. 12 The Reciprocal Promotion and Protection of Investments between the Argentine Republic and the State of Qatar, 6 November 2016. Such provisions neither obligate states to regulate investments nor impose human rights obligations on investors.89x Choudhury, above n. 38, at 13. More stringent provisions may stipulate that ‘investors … shall strive to achieve the highest possible level of contribution to the sustainable development’.90x Art. 9(1) Investment Cooperation and Facilitation Agreement between the Federative Republic of Brazil and the Republic of Malawi, 25 June 2015. However, even though words like investors shall may indicate concrete obligations, the ambiguity and the use of words and phrases like voluntarily, strive and highest possible in the remainder of such provisions limit their stringency. Such changes in the use of words compared with softer provisions do not suffice to render these provisions more enforceable and leave a significant degree of flexibility to arbitrators when determining what such words mean.91x Yan, above n. 36, at 997. At the hard law end of the spectrum, there are provisions stating that, for example, ‘investors and investments shall act in accordance with fundamental labour standards as stipulated in the ILO Declaration on Fundamental Principles and Rights of Work, 1998’.92x Art. 14(4) ECOWAS Supplementary Act, above n. 16.

That approximately 27% of investor obligations provisions deal with CSR, sustainable development, anti-corruption and environment, labour rights and human rights protection could still be considered as a significant improvement in drafting IIAs that are more mindful of human rights issues. However, this would be significant only if these provisions had been worded in a more precise, enforceable and strict way. By looking at where these provisions are located, one could argue that since more than 73% of these specific provisions (427 out of 583) are found in the body sections of IIAs and not in their preamble, they should be easily enforceable. Yet 84% of these provisions (492 out of 583) can be considered aspirational or hortatory, formulated broadly and imposing no clear obligations on investors. Moreover, most of these provisions (336 out of 583) do not directly address investors. Furthermore, they also contain many ambiguities, such as what encouragement of investors or internationally recognised CSR standards mean. In total, there are only 70 provisions dealing with these subjects, directly addressed to investors, and they are mandatory in their language.

It may be argued that such hortatory and aspirational provisions can offer certain benefits. These provisions may incorporate public policy goals such as promoting sustainable development or responsible investments into the objects and purposes of an IIA. This, in turn, may lead arbitrators to strive more to strike a balance between the interests of investors and those of states. By providing a more solid base, these provisions could also encourage arbitrators to apply the clean hands doctrine to require investors to have acted in good faith throughout their investments and not be involved in any wilful wrongdoing.93x D. Gaukrodger, ‘Business Responsibilities and Investment Treaties’, OECD Working Papers on International Investment 2021/02, at 105. Additionally, these provisions could allow states to differentiate between responsible and irresponsible investments for the purposes of standards of national treatment or most-favoured-nation by providing a basis for the finding that such investments are not in like circumstances.94x Ibid., 104. However, these potential benefits are conditional on how arbitrators interpret these softer, hortatory and aspirational provisions. Considering the tilt of the rules and structure of investment law in favour of investors,95x D. Schneiderman, ‘Global Constitutionalism and Its Legitimacy Problems: Human Rights, Proportionality, and International Investment Law’, 12 The Law & Ethics of Human Rights 251, at 261 (2018). reliance on arbitrators’ interpretations to encourage responsible investment is unsuitable for this purpose.